2. Dun & Bradstreet (D&B) — Top Coface Competitor for Business Credit Reports, Payment Data & Global Risk Intelligence

Dun & Bradstreet (D&B) is one of the most established global providers of business credit reports, payment behavior intelligence, and commercial risk scoring. With decades of historical data and a broad international footprint, it is frequently evaluated as a leading alternative to Coface—especially for organizations that prioritize credit decisioning, trade payment insight, and portfolio risk monitoring.

Dun & Bradstreet (D&B) is one of the most established global providers of business credit reports, payment behavior intelligence, and commercial risk scoring. With decades of historical data and a broad international footprint, it is frequently evaluated as a leading alternative to Coface—especially for organizations that prioritize credit decisioning, trade payment insight, and portfolio risk monitoring.

About Dun & Bradstreet: What This Coface Alternative Offers for Company Credit & Risk Assessment

Dun & Bradstreet provides a wide portfolio of business credit and risk tools, including credit reports, risk indicators, global business profiles, and compliance screening. Its D-U-N-S® Number system is one of the most widely used business identifiers for KYB, supplier onboarding, and financial verification.

D&B strengthens its offering with trade payment data (Paydex), industry benchmarking, predictive analytics, and identity resolution services. It is commonly used by finance teams, credit analysts, banks, government agencies, and procurement teams.

Key Strengths of Dun & Bradstreet for Credit Risk, Payment Behavior & Business Verification

1. Global Brand Reputation & Long Historical Coverage

D&B is one of the most recognized names in the commercial credit and risk industry, trusted by banks and enterprises worldwide.

2. D-U-N-S® Number as a Standard Global Identifier

Adopted by governments, financial institutions, and Fortune 500 organizations for onboarding, supplier checks, and KYB processes.

3. Extensive Trade Payment Insights (Paydex)

The Paydex score is one of the industry’s most valuable metrics for understanding payment behavior and predicting delays.

4. Broad International Network & Data Supply

D&B maintains global coverage through partnerships and long-standing data acquisition programs.

5. Strong Compliance Screening Capabilities

The platform includes sanctions, watchlists, PEP checks, and AML screening tools needed for compliance workflows.

Weaknesses of Dun & Bradstreet Compared to Other Coface Alternatives

1. Heavy Dependence on External Data Providers

In many markets, D&B does not collect data directly from registries and instead relies on local partners, leading to inconsistencies in:

accuracy

freshness

data depth

ownership records

2. Limited Transparency Into Original Data Sources

D&B does not typically show which registry or official source each data point came from.

3. Restrictive Licensing & Resale Rights

D&B has some of the strictest data licensing rules in the industry. Customers are limited in:

4. Pricing Is Often Higher Than Comparable Providers

Enterprise contracts can become costly—especially for global usage, API access, or bulk data requests.

5. Limited UBO, Shareholder & Corporate Structure Depth

D&B provides some ownership data, but coverage can be shallow and inconsistent compared to registry-based data providers.

Dun & Bradstreet vs. Coface: Business Credit Data, Payment Insights & Risk Intelligence Compared

Feature / Capability | Dun & Bradstreet | Coface |

|---|

Primary Focus | Credit reports, payment data, global risk scores | Trade credit insurance, business credit reports |

Payment Insights | Extensive (Paydex score) | Yes |

Financial Data | Partial, varies by region | Partial |

Ownership Data (UBO) | Limited depth | Very limited |

Corporate Group Structures | Basic mapping | Minimal |

API Access | Available | Limited structured delivery |

Bulk Data Licensing | Restricted | Not supported |

Data Collection Model | Mixed (partners + internal) | CEE internal, rest external |

Ideal Use Case | Credit decisioning & supplier risk | Credit insurance & basic credit checks |

Is Dun & Bradstreet a Good Coface Alternative? Final Verdict

Dun & Bradstreet is a strong alternative to Coface for companies seeking traditional business credit reports, payment behavior data, and global risk scoring. Its long history and widespread use of the D-U-N-S® Number make it a trusted player for credit analysis and supplier verification.

However, limitations around data transparency, licensing restrictions, ownership depth, and cost mean that many businesses evaluate additional competitors—particularly if they require registry-sourced data, UBO mapping, flexible data licensing, or large-scale enrichment capabilities.

Frequently Asked Questions About Dun & Bradstreet as a Coface Alternative

1. What makes Dun & Bradstreet a viable alternative to Coface for business credit data?

Dun & Bradstreet offers global business credit reports, payment behavior data, and commercial risk scoring. Companies choose it as a Coface alternative when they need broader payment insights or long-established credit rating methodologies.

2. Does Dun & Bradstreet provide detailed payment performance data?

Yes. D&B’s Paydex score and payment history database are among the most widely used indicators for assessing payment reliability and predicting potential delays.

3. How accurate and transparent is Dun & Bradstreet’s company data?

Accuracy varies by region. In many countries, D&B sources data through local partners rather than directly from official registries, which can affect transparency into the original source of information.

4. Does Dun & Bradstreet include UBO and shareholder information?

D&B offers ownership information, but coverage depth depends on the country. It does not consistently provide full UBO visibility or detailed shareholder structures across all jurisdictions.

5. Are there usage or licensing limitations when working with Dun & Bradstreet data?

Yes. Dun & Bradstreet imposes strict licensing rules that limit redistribution, bulk storage, derivative products, and open embedding of its data in external applications.

3. Zephira.ai — Modern Coface Alternative for KYB APIs, Registry Data & Real-Time Company Verification

Zephira.ai is an API-first KYB and company data platform offering real-time access to registry-verified company information, ownership structures, financial filings, and director data across global markets. It is designed for fintechs, compliance teams, onboarding platforms, and B2B applications that require structured, real-time company intelligence, not traditional credit reports.

Zephira.ai is an API-first KYB and company data platform offering real-time access to registry-verified company information, ownership structures, financial filings, and director data across global markets. It is designed for fintechs, compliance teams, onboarding platforms, and B2B applications that require structured, real-time company intelligence, not traditional credit reports.

Zephira.ai is a strong Coface alternative for organizations that want raw registry data to power their own credit decisioning, KYB checks, risk models, and onboarding automation.

About Zephira.ai: API Platform for Registry-Sourced Company, Ownership & Filing Data

Zephira.ai consolidates official government registry information into a unified, standardized API, enabling instant access to:

Legal company profiles

Registration numbers & tax identifiers

Financial statements (digitized & normalized)

Directors & management data

Shareholders & ownership layers

UBO mapping & group structures

Registry filings & corporate documents

Status changes, incorporations & dissolutions

Sanctions, watchlist & compliance checks

It focuses entirely on verifiable official data — the same type of raw information used by credit bureaus to build scoring models.

Key Strengths of Zephira.ai for KYB, Onboarding Automation & Entity Verification

1. API-First Architecture for Real-Time KYB & Entity Checks

Built for automated workflows, risk engines, and platforms that require instant, structured company data.

2. Direct Registry-Sourced Business Information

All core company data originates from official business registries, ensuring accuracy for compliance and verification.

3. Detailed Ownership Structures & UBO Visibility

Provides multi-level shareholder information, ownership paths, UBO mapping, and full group structure insights.

4. Financial Statements Digitized with OCR + AI

Zephira.ai converts global registry filings into normalized financial statements suitable for modeling and analysis.

5. Developer-Friendly, High-Volume API Consumption

Supports bulk enrichment, onboarding flows, CRM updates, transaction monitoring, and automated verification pipelines.

Weaknesses of Zephira.ai Compared to Coface

1. No Credit Scores or Risk Models

Zephira.ai does not generate credit scores or commercial risk ratings.

It only provides the underlying data that risk engines use to produce such scores.

2. No Trade Payment Data

Unlike Coface or D&B, Zephira.ai does not include DBT metrics, payment experiences, or trade lines.

3. No Trade Credit Insurance

Zephira.ai does not offer credit insurance or loss protection services.

4. No Traditional PDF Credit Reports

Designed for API delivery — not for downloading PDF credit reports.

5. Financial Detail Depends on Local Registry Disclosure

Jurisdictions with limited public reporting will have less available data.

Zephira.ai vs. Coface — Registry Data, KYB, Ownership & Compliance Features Compared

Category | Zephira.ai | Coface |

|---|

Primary Strength | Real-time registry-sourced company data via API | Credit insurance and business credit reports |

Geographical Strength | 100+ official registries globally | Strong in Europe, especially CEE |

Registry-Verified Company Profiles | Yes — sourced directly from government registers | Partial — relies on partners for many markets |

Financial Statements | Available when published by registries | Partial, varies by country |

Ownership & Shareholder Data | Yes — registry-sourced ownership layers | Very limited ownership information |

UBO Intelligence | Basic logical tracing (no credit scoring) | Very limited UBO visibility |

Credit Scores / Credit Limits | Not provided | Strong credit scoring tied to insurance models |

Trade Payment Data (DBT) | Not available | Moderate payment behavior insights |

API Access | Strong, developer-first API for real-time lookups | Report-based API with limited flexibility |

Bulk Data / Redistribution Rights | Available for registry datasets | No bulk resale or redistribution allowed |

Ideal Use Case | KYB, entity verification, registry data enrichment | Credit insurance, supplier risk assessment |

Conclusion

Zephira.ai is a powerful alternative to Coface for companies that need real-time registry data, ownership intelligence, and API-based KYB automation. It is not a credit bureau and does not produce credit scores — but it provides the raw legal, financial, and ownership data that risk teams and credit bureaus rely on to build their decisioning models.

For compliance teams, onboarding platforms, fintechs, and developers seeking accurate, structured, and scalable company data, Zephira.ai offers far more flexibility and technical depth than traditional report-based providers like Coface.

Frequently Asked Questions About Zephira.ai as a Coface Alternative

1. What makes Zephira.ai different from Coface?

Zephira.ai provides real-time registry data through an API, including legal information, filings, ownership, and UBO structures. Coface provides credit reports and credit insurance. Zephira.ai is used to power KYB, onboarding, and compliance workflows, while Coface is geared toward credit decisioning and invoice protection.

2. Does Zephira.ai offer credit scores or payment behavior data?

No. Zephira.ai does not provide credit scores, DBT metrics, or payment insights. It focuses solely on verified registry data, which businesses can use to build their own scoring or risk models.

3. Can Zephira.ai be used for automated KYB and compliance checks?

Yes. Zephira.ai provides the core information required for KYB and AML processes, including company identity, tax IDs, financial filings, directors, shareholders, and UBO data.

4. Does Zephira.ai include global ownership and UBO intelligence?

Yes. The platform provides multi-level shareholder data, ownership chains, and beneficial owner visibility, making it suitable for financial crime prevention and enhanced due diligence.

5. Is Zephira.ai suitable for onboarding platforms and fintech integrations?

Yes. Zephira.ai is designed for high-volume API integrations, making it ideal for onboarding tools, compliance systems, CRMs, and fintech applications that need fast, structured entity data

4. Creditsafe — Popular Coface Alternative for Business Credit Reports, Company Scores & Trade Payment Insights

Creditsafe is one of the most widely used commercial credit reporting companies in the world, offering business credit scores, company reports, and trade payment behavior across millions of companies. It is commonly considered a strong alternative to Coface, especially for teams that need fast access to traditional credit data rather than registry-level ownership structures or API-ready company intelligence.

Creditsafe is one of the most widely used commercial credit reporting companies in the world, offering business credit scores, company reports, and trade payment behavior across millions of companies. It is commonly considered a strong alternative to Coface, especially for teams that need fast access to traditional credit data rather than registry-level ownership structures or API-ready company intelligence.

About Creditsafe: What This Coface Competitor Offers for Business Credit Reports & Risk Analysis

Creditsafe provides global business credit reports, credit scores, recommended credit limits, payment trends, DBT data, and negative event monitoring.

Its platform is designed to help companies assess customer risk, approve new accounts, prevent bad debt, and screen suppliers.

Creditsafe’s global network covers many markets, though the depth of information varies by country. The company also integrates trade payment data and financial ratios into its scoring models, making it useful for operational credit teams.

Key Strengths of Creditsafe for Credit Reports, Payment Behavior & Business Risk Assessment

Fast, Easy-to-Use Global Credit Reports

Creditsafe is known for its simple interface, quick company lookups, and easy-to-read business credit summaries.

Business Credit Scores & Recommended Credit Limits

Credit risk scoring models help users gauge risk quickly and decide how much credit to extend to a customer.

Extensive Trade Payment Data

Creditsafe collects DBT metrics and payment experiences from global partners, providing insights into how reliably a company pays invoices.

Affordable Pricing Relative to Other Credit Bureaus

Often more cost-effective than D&B or Coface for companies needing frequent credit checks.

Negative Event Monitoring

Includes alerts on changes in financial stability, late payments, legal issues, insolvencies, and business closures.

Weaknesses of Creditsafe Compared to Other Coface Alternatives

Heavy Reliance on Third-Party Data in Many Countries

Creditsafe sources much of its global data through external partners.

Coverage depth varies significantly from country to country.

Limited UBO, Shareholder & Registry-Level Transparency

Creditsafe provides minimal ownership data and does not offer registry filings, UBO structures, or multi-layer group relationships.

No Access to Full Registry Filings or Documents

Unlike registry-based providers, Creditsafe does not supply original corporate filings or official registry documents.

Restricted Data Licensing & Bulk Usage

Creditsafe does not support broad redistribution or large-scale data licensing for building analytics models or powering external applications.

Depth of Financial Data Varies Widely

In some countries, financial statements may be missing or heavily summarized.

Creditsafe vs. Coface — Business Credit Reports, Payment Insights & Risk Data Compared

Category | Creditsafe | Coface |

|---|

Primary Strength | Fast, standardized business credit reports & credit scores | Credit insurance and global credit risk reporting |

Geographical Strength | Strong in Europe, UK, US | Strong in Europe, especially CEE |

Commercial Credit Scores | Yes — widely used for operational credit checks | Yes — tied to credit insurance assessments |

Trade Payment Data (DBT) | Strong trade payment data & DBT metrics | Moderate payment behavior coverage |

Financial Statements | Available in some markets; varies by region | Partial, depending on local registry availability |

Negative Events (Court Actions, Insolvencies) | Available in many countries | Available in many countries |

Ownership & UBO Transparency | Limited ownership information | Very limited ownership data |

Data Licensing & Resale Rights | Highly restricted; no bulk or resale allowed | Restricted; no resale allowed |

API Access | Available, focused on credit reports | Report-based API with limited flexibility |

Ideal Use Case | Quick business credit checks & payment risk evaluation | Credit insurance, international credit risk reporting |

Conclusion

Creditsafe is a strong Coface alternative for organizations that prioritize traditional business credit reports, quick scoring, and trade payment insights. Its platform is user-friendly, globally recognized, and often more cost-effective than larger credit bureaus.

However, businesses needing registry-verified data, UBO mapping, full ownership structures, or detailed corporate filings will find Creditsafe less suitable compared to more modern, registry-based alternatives.

Frequently Asked Questions About Creditsafe as a Coface Alternative

What makes Creditsafe a good alternative to Coface?

Creditsafe provides global business credit reports, credit scores, and payment behavior data, making it useful for operational credit checks where teams need quick, standardized assessments.

Does Creditsafe include payment performance and DBT metrics?

Yes. Creditsafe offers Days Beyond Terms (DBT) data and trade payment experiences, helping users identify late payers and assess financial reliability.

How detailed is Creditsafe’s ownership and shareholder information?

Ownership depth is limited. Creditsafe focuses on credit scoring and payment data, not on providing full shareholder records, UBO structures, or registry filings.

Can Creditsafe be used for KYB or compliance verification?

Only at a basic level. Creditsafe can confirm company existence and basic identifiers, but it does not offer the registry-level detail required for deeper KYB, AML, or enhanced due diligence.

Does Creditsafe allow access to bulk company data or large-scale datasets?

No. Creditsafe has strict licensing restrictions and does not allow bulk data extracts, redistribution, or the creation of derivative data products.

5. CRIF — Major Coface Alternative for Credit Reports, Financial Statements & Risk Management Solutions

CRIF is one of the largest global providers of business credit reports, financial statements, risk scoring models, and credit management solutions, with a strong presence across Europe, especially Italy, Central Europe, and Asia. It is frequently evaluated as a top alternative to Coface for organizations that need deep credit insights, financial analysis, and integrated risk decisioning tools.

CRIF is one of the largest global providers of business credit reports, financial statements, risk scoring models, and credit management solutions, with a strong presence across Europe, especially Italy, Central Europe, and Asia. It is frequently evaluated as a top alternative to Coface for organizations that need deep credit insights, financial analysis, and integrated risk decisioning tools.

About CRIF: What This Coface Competitor Offers for Business Credit Risk & Financial Reliability

CRIF provides a broad suite of credit intelligence solutions, blending business credit reports, company financials, credit scoring, payment behavior, risk decisioning engines, and portfolio management platforms.

Its commercial credit reports include:

Credit scores

Credit limits

Financial ratios & statements

Payment behavior data

Legal events & negative filings

Insolvency indicators

Company identity information

Industry benchmarking

CRIF is also known for its strong analytics capabilities and predictive models used by banks, lenders, and financial institutions.

Key Strengths of CRIF for Credit Reports, Financial Analysis & Risk Scoring

1. Strong Presence in Europe and Asia

CRIF has deep regional coverage, especially in Italy, Central Europe, and parts of Asia, supported by multiple local subsidiaries and data networks.

Detailed Financial Statements & Ratios

CRIF provides structured financial statements, financial ratios, and sector benchmarking to support credit and lending decisions.

Advanced Credit Scoring & Predictive Analytics

CRIF offers proprietary commercial credit scores and risk models widely used by banks, insurers, and credit managers.

Comprehensive Risk & Portfolio Management Platforms

Includes solutions for onboarding, underwriting, credit limit setting, portfolio monitoring, and early-warning analytics.

Legal Events, Insolvencies & Court Filings

CRIF monitors negative events and legal actions to give early signals of financial distress.

Weaknesses of CRIF Compared to Other Coface Alternatives

Limited Ownership Transparency (UBO & Shareholders)

CRIF focuses on credit data, financials, and scoring—not deep registry-based ownership or UBO mapping.

Data Sourcing Depends on Local Partners

Outside core markets, CRIF relies heavily on partner-sourced data, which can reduce consistency and visibility into original registry filings.

Restrictive Licensing for Bulk & Redistributed Use Cases

CRIF’s data is usually licensed for internal use only—making it difficult for platforms and data products to embed or resell the data.

High Cost for Advanced Credit & Risk Analytics

Enterprise-level scoring models and decision engines can be significantly more expensive than modern alternatives.

Not Ideal for Developer-Led or API-First Use Cases

CRIF is built around platforms and reports; its APIs are not as flexible as modern registry-based or developer-focused providers.

CRIF vs. Coface — Credit Reports, Financial Statements & Risk Data Compared

Feature / Capability | CRIF | Coface |

|---|

Primary Focus | Credit scoring, financial data, analytics | Credit insurance & credit reports |

Credit Scores | Yes | Yes |

Financial Statements | Strong | Partial |

Payment Behavior | Yes | Yes |

Ownership & UBO Data | Limited | Very limited |

Legal Events | Yes | Yes |

API Access | Available | Report-based API |

Bulk Data Licensing | Restricted | Not supported |

Regional Strength | Italy, CEE, Asia | CEE |

Best Use Case | Credit risk modeling & financial analysis | Trade credit insurance |

Conclusion

CRIF is a leading Coface alternative for companies seeking detailed credit reports, financial statements, credit scoring models, and advanced risk analytics. Its strong regional presence—particularly in Europe and Asia—makes it valuable for lenders and credit managers.

However, organizations needing registry-sourced ownership data, flexible licensing, or API-first company intelligence may find CRIF less suitable compared to modern, data-centric competitors.

Frequently Asked Questions About CRIF as a Coface Alternative

How does CRIF compare to Coface for business credit reporting?

CRIF offers detailed credit reports, scoring models, financial statements, and payment behavior insights—making it a strong alternative for companies focused on credit analysis rather than credit insurance.

Does CRIF include payment performance and late-payment indicators?

Yes. CRIF provides payment behavior, late-payment trends, and other signals that help assess a company’s likelihood of paying on time.

Does CRIF provide beneficial ownership or deep shareholder data?

Only partially. CRIF focuses on credit intelligence, financial data, and scoring; it does not specialize in registry-level UBO visibility or multi-layer ownership mapping.

Is CRIF suitable for underwriting, scoring, and financial risk analysis?

Yes. CRIF is widely used by banks and financial institutions for underwriting workflows, scoring models, and ongoing portfolio risk monitoring.

Can customers license CRIF data in bulk or embed it into external platforms?

No. CRIF’s licensing agreements restrict bulk usage, redistribution, and embedding data into customer-facing applications.

6. Experian — Leading Coface Alternative for Business Credit Reports, Risk Scoring & Trade Payment Insights

Experian is one of the world’s largest credit bureaus and a major provider of business credit reports, financial risk scores, payment behavior data, and negative filings. It is widely considered an alternative to Coface for companies that require commercial credit checks, portfolio monitoring, or trade payment intelligence.

Experian is one of the world’s largest credit bureaus and a major provider of business credit reports, financial risk scores, payment behavior data, and negative filings. It is widely considered an alternative to Coface for companies that require commercial credit checks, portfolio monitoring, or trade payment intelligence.

About Experian: What This Coface Competitor Provides for Business Credit & Financial Risk Assessment

Experian’s business credit solutions deliver detailed risk insights across SMEs and large enterprises, including:

Commercial credit scores

Credit limits

Company identity verification

Financial statements (in select countries)

Trade payment performance

Late payment indicators

Legal filings, liens & judgments

Bankruptcy records

Fraud and identity risk alerts

Experian’s strength lies in blending payment data, bureau data, and behavioral signals, making it popular in lending, underwriting, supplier onboarding, and credit management teams.

Key Strengths of Experian for Business Credit Intelligence & Risk Decisions

Strong Global Trade Payment Data Network

Experian aggregates supplier payment data, Days Beyond Terms (DBT), and delinquency patterns—valuable for predicting late payers.

Widely Used Commercial Credit Scores

Their credit risk models are trusted across banks, lenders, and enterprises for assessing liquidity risk and default probability.

Large Database of Negative Events & Legal Filings

Experian tracks liens, judgments, court actions, bankruptcies, and overdue filings across multiple countries.

Widely Adopted Across Lending & Underwriting Teams

Its credit bureau heritage makes Experian a strong fit for organizations that require validated credit scores and bureau-derived insights.

Integrated Fraud & Identity Risk Solutions

Experian can combine business credit checks with fraud alerts and identity risk signals for more secure customer onboarding.

Weaknesses of Experian Compared to Other Coface Alternatives

Limited Registry-Sourced Ownership & UBO Depth

Experian does not provide multi-layer ownership, beneficial ownership, or registry filings—its data is credit-focused.

Inconsistent International Coverage

Experian is very strong in the US and UK, but coverage varies widely across Europe, Asia, and emerging markets.

Strict Licensing & Redistribution Restrictions

Experian does not allow bulk data extraction or redistribution, making it unsuitable for data platforms and product enrichment.

Not Designed for API-First KYB or Compliance Use Cases

Experian is built for credit decisions—not KYB, due diligence, or registry-based verification.

Financial Data Only Available in Select Markets

Experian does not provide consistent global financials like newer registry-first platforms.

Experian vs. Coface — Business Credit Reports, Payment Data & Risk Signals Compared

Category | Experian | Coface |

|---|

Primary Strength | Commercial credit scores, bureau data & payment behavior insights | Credit insurance and global credit risk reporting |

Geographical Strength | Very strong in US & UK | Strong across Europe, especially CEE |

Commercial Credit Scores | Robust, widely used by lenders & enterprises | Strong credit scoring linked to insurance decisions |

Trade Payment Data (DBT) | Extensive DBT, payment trends & delinquency insights | Moderate payment performance coverage |

Financial Statements | Limited global coverage | Partial financials, depending on country |

Negative Events (Bankruptcies, Liens, Judgments) | Very strong | Available in many markets |

Ownership / UBO Transparency | Very limited | Very limited |

Fraud & Identity Risk Tools | Strong fraud prevention & business identity checks | Basic fraud intelligence |

API Access | Moderate API availability | Report-based API with limited flexibility |

Bulk Data & Redistribution Rights | Restricted; no resale or redistribution allowed | Also restricted; no bulk usage allowed |

Ideal Use Case | Underwriting, credit decisioning, payment risk analysis | Credit insurance, international credit reporting |

Conclusion

Experian is one of the strongest Coface alternatives for organizations that rely heavily on payment behavior data, commercial credit scores, and negative event monitoring. It is particularly valuable for lenders, credit managers, and procurement teams assessing supplier risk.

However, companies that need registry-sourced data, global ownership transparency, multi-country financials, or flexible data licensing may find Experian limited compared to more modern, registry-based providers.

Frequently Asked Questions About Experian as a Coface Alternative

How does Experian compare to Coface for business credit risk?

Experian offers strong commercial credit scores, payment behavior data, and negative filings, making it a solid alternative to Coface for ongoing credit and supplier risk monitoring.

Does Experian provide trade payment data and DBT insights?

Yes. Experian has extensive trade payment data, including Days Beyond Terms (DBT), which helps identify chronic late payers and assess cash-flow health.

Does Experian give access to UBO, shareholder, or registry-level ownership data?

No. Experian focuses on credit bureau and payment data, not registry-sourced ownership structures or UBO transparency.

Is Experian suitable for underwriting and financial risk scoring?

Yes. Experian is widely used by banks, lenders, and credit teams for risk scoring, underwriting workflows, and portfolio monitoring.

Can Experian data be licensed in bulk or used in customer-facing products?

No. Experian has strict licensing restrictions that prevent bulk exports, redistribution, or embedding data into external applications.

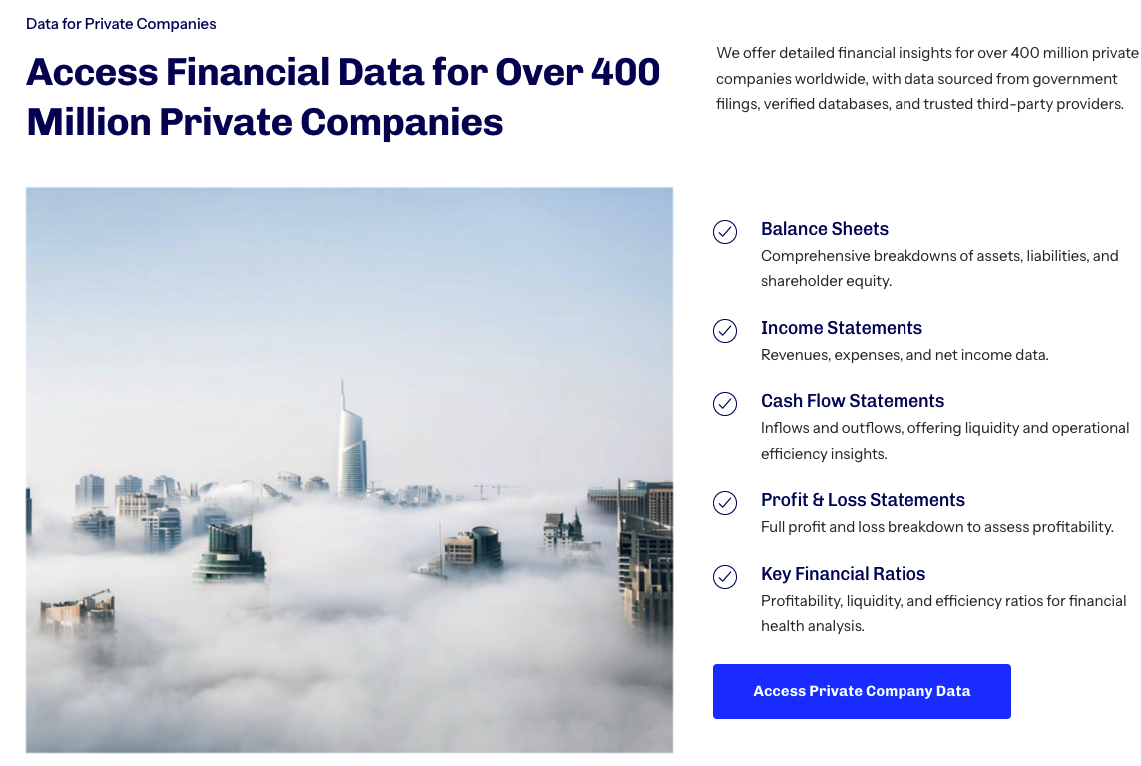

7. Monetaiq — Emerging Coface Alternative for Global Financial Statements & Company Performance Data

Monetaiq is a modern financial data platform that provides private and public company financial statements, historical performance metrics, and structured financial datasets. It is often considered alongside Coface by teams that need deep financial transparency rather than traditional credit insurance data.

Monetaiq is a modern financial data platform that provides private and public company financial statements, historical performance metrics, and structured financial datasets. It is often considered alongside Coface by teams that need deep financial transparency rather than traditional credit insurance data.

About Monetaiq: What This Coface Competitor Provides for Financial Intelligence

Monetaiq aggregates and normalizes financial data for over 400 million private companies and tens of thousands of public companies, offering:

Full financial statements (balance sheet, income statement, cash flow)

Multi-year historical data

Performance trends and financial ratios

Industry and peer comparison metrics

API and bulk data outputs for integration

Standardized data formats for analytics, modeling, and enrichment

Monetaiq is built for data teams, fintechs, analysts, and platforms requiring structured company financials at global scale.

Monetaiq Strengths for Financial Data & Company Performance Analysis

Strong Global Financial Coverage

Provides financials for hundreds of millions of companies across regions and industry sectors.

Multi-Year Historical Data for Trend Analysis

Enables long-term performance tracking, modeling, and predictive analysis.

API and Bulk Delivery Options

Designed for product enrichment, underwriting engines, financial modeling, and analytics platforms.

Detailed Statements for Private Companies

Offers structured private-company financials, which many legacy providers do not make easily accessible.

Developer-Friendly Data Structure

Clean, normalized formats that simplify integration into data pipelines and internal systems.

Monetaiq Weaknesses Compared to Coface and Other Alternatives

No Credit Scores or Credit Risk Models

Monetaiq focuses on financial data—not credit scoring, payment behavior, or risk prediction.

Limited Ownership & UBO Transparency

Does not provide shareholder trees, UBO mapping, or registry-sourced corporate linkages.

No Trade Payment Data or DBT Signals

Unlike credit bureaus, Monetaiq does not track supplier payment behavior.

Not Designed for Compliance or KYB

Does not include KYB checks, registry filings, sanctions data, or AML intelligence.

Data Depth Varies by Country

The availability of private-company financials depends on local disclosure requirements.

Monetaiq vs. Coface — Financial Data & Company Intelligence Compared

Category | Monetaiq | Coface |

|---|

Primary Strength | Global financial statements & multi-year performance data | Credit insurance and international credit reports |

Company Coverage | 400M+ private companies + public companies worldwide | Strong in Europe, especially CEE |

Financial Statements | Extensive, structured, multi-year financials | Partial, varies by country |

Historical Data | Strong long-term financial histories | Limited financial history |

Credit Scores & Credit Limits | Not available | Strong credit scoring linked to insurance models |

Trade Payment Data (DBT) | Not provided | Moderate DBT and payment behavior insights |

Ownership & UBO Data | Very limited | Very limited |

Risk & Negative Events | Not a core focus | Includes court events, insolvency indicators, business status |

API Access | Strong APIs for financial data ingestion | Basic, report-driven API |

Bulk Data Delivery | Supported for financial datasets | Not supported (no bulk resale) |

Ideal Use Case | Financial modeling, benchmarking, analytics, platform enrichment | Credit insurance, credit risk reporting, supplier risk management |

Conclusion

Monetaiq is a strong Coface alternative for teams that need global financial statements, multi-year performance trends, and structured financial data via API or bulk delivery. It is ideal for fintechs, data teams, investment analysts, and platforms requiring consistent financial intelligence.

However, companies looking for credit scores, payment behavior, KYB, or ownership transparency will find Monetaiq less suitable than risk-oriented competitors.

Frequently Asked Questions About Monetaiq as a Coface Alternative

How does Monetaiq compare to Coface for company insight?

Monetaiq focuses on delivering global financial statements and historical performance data, while Coface specializes in credit insurance and credit risk reporting. They serve different needs.

Does Monetaiq provide full financial statements for private companies?

Yes. Monetaiq offers structured financial statements for a large number of private companies globally, including multi-year trends.

Does Monetaiq include credit scores or payment behavior data?

No. Monetaiq does not offer credit scoring, trade payment data, or DBT metrics.

Does Monetaiq provide registry-sourced ownership or UBO information?

No. Monetaiq does not include shareholder trees, UBO data, or registry filings. Its focus is financial performance, not corporate structures.

Can Monetaiq be integrated into platforms via API or bulk data files?

Yes. Monetaiq supports API access and bulk delivery formats designed for analytics platforms, enrichment workflows, and data products.

8. Equifax — Major Coface Alternative for Business Credit Scores, Payment Data & Fraud Risk Intelligence

Equifax is one of the world’s largest credit bureaus and a significant provider of business credit scores, payment behavior data, commercial credit reports, fraud prevention tools, and identity risk signals.

Equifax is one of the world’s largest credit bureaus and a significant provider of business credit scores, payment behavior data, commercial credit reports, fraud prevention tools, and identity risk signals.

It is often evaluated as a Coface alternative by teams that need credit decisioning, supplier risk checks, or commercial credit assessments, especially in the US, Canada, and the UK.

About Equifax: What This Coface Competitor Offers for Business Credit & Commercial Risk Evaluation

Equifax provides a wide range of credit intelligence solutions used by lenders, banks, insurers, and procurement teams.

Its business credit reports typically include:

Commercial credit scores

Credit limits

Trade payment behavior

DBT (Days Beyond Terms) indicators

Public filings, legal events, liens & judgments

Bankruptcy and insolvency data

Fraud and identity risk signals

Business identity verification

Equifax is widely adopted in underwriting, credit decisioning, onboarding, and supplier risk workflows.

Equifax Strengths for Commercial Credit Risk & Payment Behavior Analysis

Strong Trade Payment Data & DBT Metrics

Equifax aggregates large volumes of payment performance data, helping predict whether a company will pay late or default.

Widely Trusted Commercial Credit Scores

Equifax scores are used across financial institutions and enterprises to assess business creditworthiness.

Deep Negative Event & Legal Filing Coverage

Includes liens, court judgments, bankruptcies, overdue filings, and other risk indicators.

Integrated Fraud & Identity Risk Solutions

Equifax is strong in fraud detection, identity validation, and verifying the legitimacy of a business.

Large Market Presence in North America

Especially strong in the US and Canada, making it a top choice for regional credit risk evaluations.

Equifax Weaknesses Compared to Other Coface Alternatives

Limited Ownership & UBO Transparency

Equifax does not provide registry-sourced shareholder data or multi-layer beneficial ownership structures.

Inconsistent International Coverage

Outside North America, coverage depth varies significantly across countries.

No Registry Filings or Document-Level Transparency

Does not provide original registry documents or access to official filings.

Restrictive Licensing & No Bulk Redistribution Rights

Equifax does not allow customers to export large datasets or embed data into external products.

Not Designed for KYB or Compliance-Driven Use Cases

Equifax focuses on commercial credit, not KYB, AML, or corporate structure verification.

Equifax vs. Coface — Credit Scores, Payment Data & Business Risk Compared

Category | Equifax | Coface |

|---|

Primary Strength | Commercial credit scores, payment behavior, and bureau risk data | Credit insurance and international credit reports |

Geographical Strength | Very strong in North America (US & Canada) | Strong across Europe, particularly CEE |

Commercial Credit Scores | Robust, widely used in lending & underwriting | Strong, tied to credit insurance models |

Trade Payment Data (DBT) | Extensive DBT and payment performance dataset | Moderate payment behavior data |

Financial Statements | Limited, varies by country | Partial coverage, depending on registry availability |

Negative Events (Liens, Judgments, Bankruptcy) | Very strong | Available in many countries |

Ownership & UBO Data | Very limited | Very limited |

Fraud & Identity Risk Tools | Strong fraud and identity verification products | Basic fraud intelligence |

API Access | Moderate API capabilities | Report-based API with limited flexibility |

Bulk Data & Redistribution Rights | Highly restricted; no bulk or resale rights | Also restricted, no resale rights |

Best Use Case | Underwriting, credit checks, payment risk analysis | Credit insurance, international credit evaluation |

Conclusion

Equifax is a strong Coface alternative for companies that need commercial credit scores, payment behavior data, and negative event intelligence, particularly in North America.

It is ideal for lenders, procurement teams, and financial institutions that rely heavily on credit bureau data when assessing business risk.

However, organizations requiring registry-sourced ownership data, multi-country financials, global coverage, or flexible licensing rights may find Equifax less suitable compared to modern data providers.

Frequently Asked Questions About Equifax as a Coface Alternative

How does Equifax compare to Coface for business credit checks?

Equifax provides strong commercial credit scores, payment data, and negative filings, making it a solid alternative to Coface for day-to-day credit risk assessment.

Does Equifax offer trade payment behavior or DBT insights?

Yes. Equifax has extensive payment performance data, including Days Beyond Terms (DBT), which helps identify late-paying or high-risk companies.

Does Equifax include ownership, shareholder, or UBO information?

No. Equifax focuses on credit bureau intelligence and does not provide registry-sourced ownership structures or UBO data.

Is Equifax used for underwriting and credit decisioning?

Yes. Equifax is widely used by lenders, banks, and enterprises to support credit scoring, underwriting workflows, and ongoing portfolio monitoring.

Can Equifax data be licensed in bulk or integrated into external platforms?

No. Equifax has strict licensing limitations and does not permit bulk redistribution or embedding data into customer-facing products.

9. Moody’s Bureau van Dijk (Orbis) — Leading Coface Alternative for Global Company Data, Corporate Structures & Financials

Moody’s Bureau van Dijk (BvD), best known for its Orbis platform, is one of the world’s most comprehensive databases for company information, ownership structures, financial statements, and corporate linkages.

Moody’s Bureau van Dijk (BvD), best known for its Orbis platform, is one of the world’s most comprehensive databases for company information, ownership structures, financial statements, and corporate linkages.

It is widely considered a premium Coface alternative by banks, insurers, researchers, and enterprises that need deep corporate intelligence, not just credit reports.

About Moody’s BvD (Orbis): What This Coface Competitor Provides

Moody’s BvD compiles data from thousands of official sources, including registries, filings, regulatory reports, and partner networks. Typical Orbis data includes:

Detailed financial statements (10+ years in many countries)

Standardized financials and ratios

Corporate hierarchy & global group structures

Ultimate beneficial owners (UBO)

Ownership percentages & shareholder trees

PEPs, sanctions, AML lists (via Compliance Catalyst)

Industry classification, company identifiers, registration numbers

M&A, investment & deal activity

It is one of the most data-rich platforms globally for entity intelligence.

Moody’s BvD Strengths for Corporate Intelligence & Financial Transparency

Deep Ownership Structures & UBO Mapping

Orbis is arguably the strongest platform globally for multi-level ownership mapping, UBO identification, and group linkage visualization.

Very Large Global Database

Hundreds of millions of companies with consistent standardization across countries.

Long Historical Financial Data

Detailed financial statements with many years of history, ideal for modeling and risk analysis.

AML, KYC & Compliance Tools

Compliance Catalyst supports sanctions screening, PEP checks, and enhanced due diligence workflows.

Powerful Search Filters & Analytics Modules

Advanced filters make Orbis popular for research, academic use, banking, consulting, and risk modeling.

Moody’s BvD Weaknesses Compared to Coface and Other Competitors

Very High Cost

Moody’s BvD is one of the most expensive data platforms in the market.

Data Freshness Varies by Country

Although data is broad, some regions rely heavily on partners rather than direct registry integrations.

Limited Trade Payment Data

Unlike credit bureaus or Coface, BvD does not offer DBT metrics or supplier payment behavior at scale.

Restricted Licensing & No Bulk Redistribution

BvD does not allow redistribution, resale, or embedding Orbis data into customer-facing platforms.

Not Designed for Real-Time API Use Cases

APIs exist but are not optimized for high-frequency, real-time queries like modern registry-first providers.

Moody’s BvD (Orbis) vs. Coface — Side-by-Side Comparison

Category | Moody’s BvD (Orbis) | Coface |

|---|

Primary Strength | Global corporate intelligence: ownership, UBO, and financial transparency | Credit insurance and business credit risk reporting |

Company Coverage | Extremely broad — hundreds of millions of entities worldwide | Strong in CEE and Europe, moderate global reach |

Financial Statements | Deep, multi-year, standardized financials | Partial financial data depending on country |

Ownership & UBO Mapping | Market-leading multi-level ownership structures & shareholder trees | Very limited ownership data |

Corporate Group Structures | The strongest global database for corporate linkages | Basic corporate hierarchy data |

Credit Scores & Risk Models | Limited business scoring; not bureau-based | Strong credit risk scoring and credit limit recommendations |

Trade Payment Data (DBT) | Minimal | Moderate — stronger than BvD |

Compliance & AML Tools | Strong — sanctions, PEPs, adverse media via Compliance Catalyst | Basic compliance checks |

API Capability | Available, but not optimized for real-time use | Report-based API; limited flexibility |

Bulk Data / Redistribution | Strictly restricted; no redistribution rights | Restricted; no bulk resale allowed |

Ideal Use Case | Corporate intelligence, UBO, M&A analysis, due diligence, research | Credit insurance, credit reporting, supplier risk assessment |

Conclusion

Moody’s Bureau van Dijk (Orbis) is one of the most powerful global company intelligence platforms available today.

It excels in ownership mapping, group structures, standardized financials, and compliance data, making it a top Coface alternative for financial institutions, researchers, and analysts.

However, companies needing credit risk signals, payment behavior, flexible licensing, or real-time API delivery may find it less suitable than specialized credit-focused or registry-first providers.

Frequently Asked Questions About Moody’s BvD as a Coface Alternative

What’s the difference between Moody’s BvD, Bureau van Dijk, and Orbis?

Bureau van Dijk (BvD) is the company name, now owned by Moody’s.

Orbis is their flagship global company database.

Is Moody’s BvD a strong alternative to Coface?

Yes—especially for ownership, corporate structures, and historical financial data. Coface is stronger in credit insurance and payment risk.

Does Moody’s BvD include UBO and shareholder mapping?

Yes. Orbis provides world-leading ownership and UBO structures across multiple levels.

Does Moody’s BvD provide credit scores or trade payment data?

Partial financial risk models yes, but no large-scale trade payment or DBT data, unlike Coface.

Can Orbis data be licensed in bulk or resold?

No. Moody’s BvD has strict licensing rules that prohibit redistribution or embedding data into external products.

Complete Comparison Table: Best Coface Alternatives in 2026

Category | Global Database | Dun & Bradstreet | Zephira.ai | Creditsafe | CRIF | Experian | Equifax | Monetaiq | Moody’s BvD (Orbis) | Creditreform | Coface |

|---|

Primary Strength | Registry-sourced global company data, UBO, financials & credit risk | Global business data & credit intelligence | Real-time registry data API | Fast credit reports | Financial statements & credit analytics | Credit bureau data & payment insights | Commercial credit scores & fraud tools | Global financial statements | Corporate ownership, UBO & financial transparency | European credit reports & collections | Credit insurance & international reports |

Data Source Type | First-party registry | Aggregated + bureau + registry partners | Direct registry | Aggregated | Mixed (strong local data in CEE/Italy) | Bureau & trade data | Bureau & trade data | Financial filings | Aggregated global registry & partners | Local registries + credit data | Mixed (partners + registry) |

Company Coverage | 600M+ profiles (200+ countries) | ~500M globally | 100+ registries | Strong global SMB coverage | Strong CEE/Italy | Very strong in US/UK | Very strong in US/Canada | 400M+ private + public | Hundreds of millions globally | Strong in Europe (Germany focus) | Strong in CEE & Europe |

Financial Statements | Yes (registry-sourced + OCR) | Yes | When registries publish | Limited by region | Strong | Limited | Limited | Strong, multi-year | Very strong, multi-year | Moderate | Partial |

Credit Scores / Limits | Yes | Yes | No | Yes | Yes | Yes | Yes | No | Partial | Yes | Yes (core strength) |

Trade Payment Data (DBT) | Moderate | Strong | No | Strong | Yes | Strong | Strong | No | Minimal | Moderate | Moderate |

Ownership / Shareholders | Strong registry ownership | Moderate | Registry-based | Limited | Limited | Very limited | Very limited | None | Very strong | Limited | Very limited |

UBO Mapping | Yes | Partial | Basic | Limited | Limited | No | No | No | Strongest globally | Limited | Very limited |

Corporate Linkages | 378M+ mapped | Strong | Limited | Limited | Moderate | Limited | Limited | None | Strongest global | Moderate | Limited |

Legal Events / Court Filings | Yes | Yes | No | Yes | Yes | Yes | Yes | No | Partial | Yes | Yes |

Compliance / KYB / AML | Strong | Moderate | Strong KYB | Basic | Moderate | Basic | Strong ID/fraud | No | Strong (Compliance Catalyst) | Moderate | Basic |

API Access | Strong | Strong | Strong | Available | Available | Moderate | Moderate | Strong | Available | Moderate | Report-based |

Bulk Delivery / Redistribution | Yes (flexible) | No | Yes | No | No | No | No | Yes | No | Limited | No |

Ideal Use Case | KYB, UBO, credit risk, platform enrichment | Enterprise credit risk, hierarchy, global data | KYB, entity verification, APIs | Operational credit checks | Financial risk analysis | Underwriting & payment risk | Credit bureau risk & fraud | Financial modeling & analytics | Ownership mapping, M&A, due diligence | Credit reports in Europe | Credit insurance & risk reports |

Conclusion: Choosing the Best Coface Alternative in 2026

The market for business credit risk, financial intelligence, and company verification has evolved far beyond traditional credit insurance. While Coface remains a strong player for international credit reports and trade credit insurance, businesses today require faster data delivery, deeper transparency, and more flexible access models.

The alternatives reviewed in this guide highlight a major shift in 2026:

Registry-sourced data providers like Global Database and Zephira.ai deliver real-time KYB, ownership structures, and financial filings that outperform legacy data workflows.

Credit bureaus such as Experian, Equifax, and Creditsafe lead in payment behavior, DBT metrics, and operational credit decisioning.

Financial data specialists like Monetaiq provide multi-year financial statements and deep performance analytics for modeling and investment use cases.

Corporate intelligence platforms like Moody’s Bureau van Dijk (Orbis) remain unmatched for ownership transparency, UBO mapping, and global group structures.

Regional risk providers such as CRIF and Creditreform excel in local depth, court filings, and SME credit data.

Ultimately, the “best” Coface alternative depends on your priority:

Credit risk & payment behavior: Choose Experian, Equifax, Creditsafe, or CRIF

KYB, registry data & UBO transparency: Choose Global Database or Zephira.ai

Financial statements & modeling: Choose Monetaiq or Moody’s BvD

Collections or regional SME risk: Choose Creditreform

Credit insurance alternatives: Combine Global Database + bureau data for underwriting

Companies in 2026 are moving toward data ownership, transparency, and API-first delivery.

Selecting a Coface alternative requires matching your use case—credit risk, compliance, onboarding, market analysis, or financial intelligence—to the provider best equipped for that need.

Top 10 Frequently Asked Questions About Coface Alternatives in 2026

What are the best Coface alternatives for global business credit reports in 2026?

The top Coface alternatives include: Global Database, Dun & Bradstreet, Creditsafe, Experian, Equifax, CRIF, Zephira.ai, Monetaiq, Moody’s Bureau van Dijk (Orbis), and Creditreform. Each offers different strengths depending on your credit, financial, or compliance needs.

Which Coface alternative provides the most accurate credit scores and payment behavior data?

Creditsafe, Experian, Equifax, and CRIF deliver the strongest credit scores, DBT insights, and payment performance data. These providers are best suited for underwriting, credit checks, and supplier risk evaluation.

Which Coface competitor offers the best registry-sourced data and company verification?

Global Database and Zephira.ai provide real-time registry-sourced company profiles, shareholder data, and KYB verification across more than 100 registries.

Which provider is strongest for ownership, UBO mapping, and corporate structures?

Moody’s Bureau van Dijk (Orbis) is the leading platform for multi-level ownership trees, global corporate linkages, and UBO insights.

What is the best Coface alternative for financial statements and historical company performance?

Monetaiq and Moody’s BvD offer the strongest multi-year financial statements and standardized financial datasets for both private and public companies.

Which Coface alternative is best for credit insurance or trade credit risk management?

While Coface specializes in credit insurance, CRIF, Creditsafe, and D&B offer strong credit risk insights that can support or supplement credit insurance workflows.

Is there a Coface alternative with flexible API access and bulk data delivery?

Global Database, Zephira.ai, and Monetaiq provide API-first access and bulk delivery options. Most traditional credit bureaus restrict bulk exports or redistribution.

Which Coface competitors are strongest in Europe?

Dun & Bradstreet, CRIF, Creditreform, and Moody’s BvD have deep European coverage. Global Database also offers extensive EU registry data and corporate linkages.

What is the difference between credit bureau providers and registry-based providers?

Credit bureaus (Experian, Equifax, Creditsafe) focus on payment behavior, credit scoring, and negative filings.

Registry-based providers (Global Database, Zephira.ai, Moody’s BvD) focus on legal data, ownership, financial filings, and entity verification.

10. How do I choose the best Coface alternative for my business needs?

Choose based on your priority:

Credit risk & DBT: Experian, Equifax, Creditsafe, CRIF

KYB & registry data: Global Database, Zephira.ai

Financial statements: Monetaiq, Moody’s BvD

European SME risk: Creditreform

Corporate intelligence: Moody’s BvD

Match your operational use case—credit checks, compliance, onboarding, analytics, or insurance—to the provider specializing in that domain.

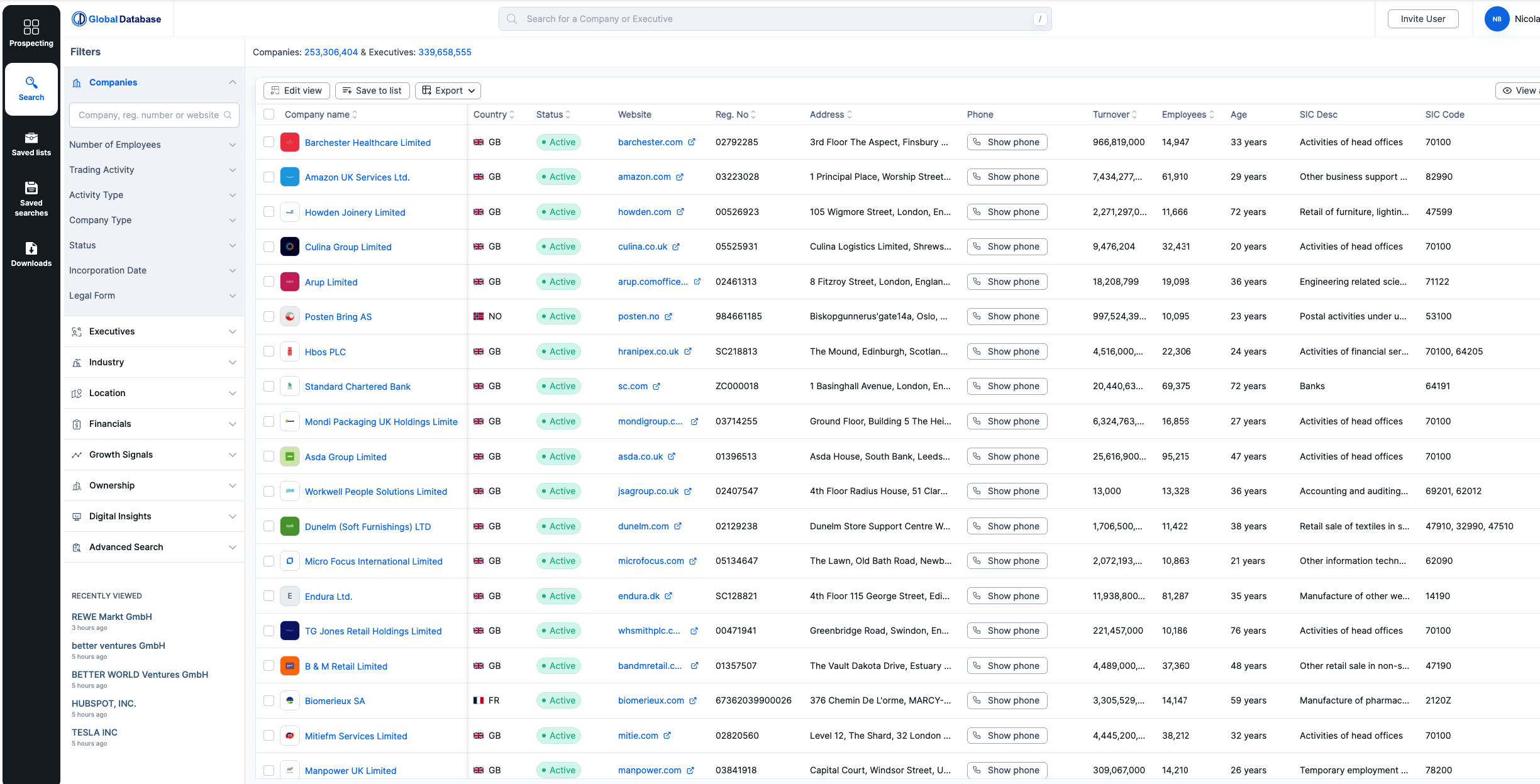

Global Database is one of the strongest alternatives to Coface for organizations requiring global credit risk data, registry-verified company information, and full ownership transparency. With more than 600M company profiles across 200+ countries, it delivers deep intelligence across legal identity, financial statements, shareholder records, UBO mapping, sanctions, court filings, and trade payment behavior—all accessible via platform and API.

Global Database is one of the strongest alternatives to Coface for organizations requiring global credit risk data, registry-verified company information, and full ownership transparency. With more than 600M company profiles across 200+ countries, it delivers deep intelligence across legal identity, financial statements, shareholder records, UBO mapping, sanctions, court filings, and trade payment behavior—all accessible via platform and API.